2026 Stock Portfolio

"Know what you own, and know why you own it." — Peter Lynch

After my first post, where I shared my top two picks that I believe will recover in 2026, I want to use this post to outline my current holdings heading into 2026 and share my perspective on each. Some stocks will get more detailed explanations than others. That said, I’ll still list all my holdings and provide insights on all my positions, particularly two stocks I’m very bullish on for the coming years. I tend to invest with a long-term mindset, usually aiming to hold stocks for at least 3–5 years, so I don’t currently have any short-term positions. Finally, I’ll share the biggest lesson I’ve learned since I started investing in 2023.

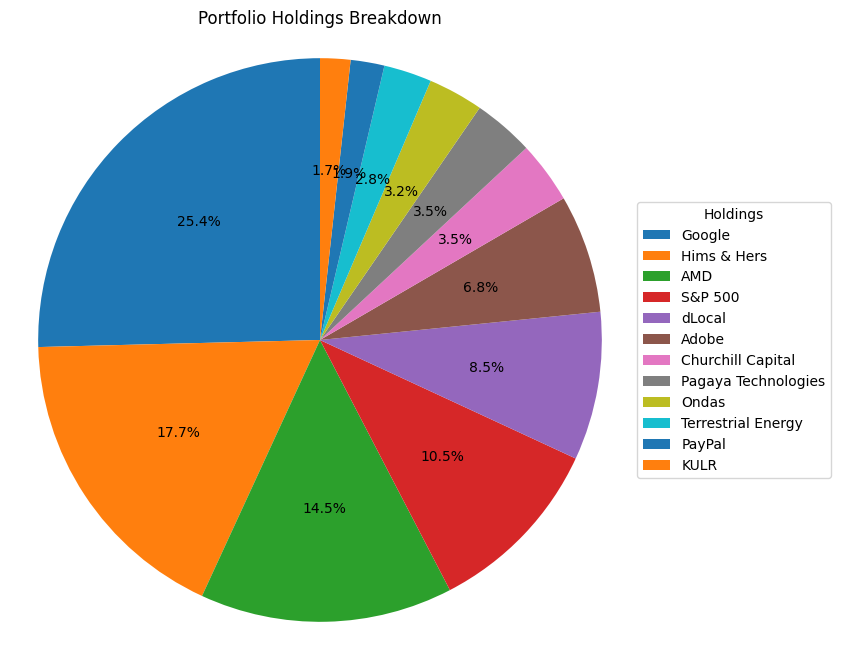

Google is currently the largest position in the portfolio. The stock was purchased in May 2025, during a period of market uncertainty following tariff comments made by Trump in April. At the time, sentiment around Google was also largely negative, driven by concerns over high AI investment costs, legal challenges, and increased competition.

Google’s AI program Gemini in my opinion it’s one of the best AI platforms out there.

The key piece of news that prompted the purchase was reports that Apple was actively exploring alternatives to Google as the default search engine on Safari, which caused significant volatility in Google’s stock. While this news led to a 5% drop in the share price on the day, the stock was already down roughly 20% from the start of 2025. In the bigger picture, it didn’t appear likely to greatly impact Google’s long-term business.

That pullback presented an attractive buying opportunity, as the valuation looked to go to be true at those levels. As of now, the position is up approximately 115% and it will be position I’ll continue holding for the long term. Throughout the holding period, portions of the position have been trimmed to build cash reserves and to average into other holdings.

My second-largest position is Hims, a stock I first bought in August 2024 and continued to actively accumulate throughout the year. Hims has easily been one of the most volatile stocks in my portfolio. I’ve trimmed shares during strong runs and added back on pullbacks as sentiment has shifted.

The company had an excellent year until the final few months, when the stock pulled back roughly 50%. I took profits around the $60 level in October, selling just over 20% of my position. Since then, the stock has continued to decline and is now down around 2% year to date. I did anticipate a pullback from $60, which is why I reduced my position at that level.

At the time, many investors were still extremely bullish, calling for $80–$100 by year-end. However, based on the company’s financials and fundamentals, I felt those expectations were overly optimistic. While I remain a strong believer in the long-term outlook for Hims, the stock had become stretched in the $60s, making a pullback reasonable in my view. That said, I didn’t anticipate the decline would be this severe, with shares falling into the $30s and recently dipping to around $28. Over the past month, I’ve being buying more shares as the valuation has become more attractive.

Hims is a prime example of a stock that was viewed as a high-growth story over the past few years. As the company has scaled, however, sustaining that level of growth has naturally become more difficult. When earnings reports show growth moderating from earlier levels, the stock can appear less attractive—especially when investors are still expecting outsized double/triple beats.

Hims is 51st most shorted stocks in the market to date, meaning many investors are betting the stock to decline. What’s surprising is that the other companies in this group are typically failing businesses—often heavily indebted and close to bankruptcy. Seeing Hims in the same category is mind-boggling to me, and it helps explain why the stock has been so volatile.

Despite this, the company continues to move in the right direction, and its financials are becoming better aligned with the stock price. Looking ahead, I believe Hims has the potential to be an $80–$100 stock, but investors will need to be patient and allow revenue and fundamentals to grow steadily alongside the share price.

As of now, my position is up 18%. Over the course of this year and years to come, I expect the stock price to continue rising as the company moves in the right direction and reach a fair and reasonable valuation. As a result, Hims remains a long-term holding for me, as I believe it has the potential to become one of the largest companies in the healthcare space.

Advanced Micro Devices (AMD) is currently my third-largest position, and it’s a stock in the semiconductor space. I originally bought AMD in December 2024, and at that time it was constantly being compared to Nvidia — usually in a negative way. The common opinion was that AMD could never compete with Nvidia, which had become the biggest company in the world by market cap.

By April, when the market pulled back during the first mention of the tariffs, AMD was hit hard. At its lowest point, I was down around 35% on the position. Sentiment online, especially on X, turned very negative. People even started calling the stock “Advanced Money Destroyer,” as many believed the company was failing to compete in the same AI and data-centre space as Nivida who was the main player during this time.

What often gets missed in this comparison is that AMD and Nvidia are playing in the same space, but they’re at very different stages. Nvidia is the clear leader in AI right now, while AMD is still earlier in its growth and execution cycle.

2025 was a massive year for AMD. One of the biggest highlights was the deal with OpenAI, where AMD will supply its AI chips to power OpenAI’s future systems. This was a major milestone because it showed that top AI companies are willing to use AMD hardware, not just Nvidia’s. For AMD, the deal boosted credibility and cemented its position as a serious player in the AI space.

Looking ahead, 2026 also looks set to be huge. Building on last year’s momentum, AMD is launching the Instinct MI400 GPUs, its next-generation AI accelerators for large-scale AI training and inference in data centres. The MI400 is a big step forward, finally putting AMD’s AI chips on a more level playing field with Nvidia’s top GPUs. I believe 2025 was just the start — 2026 could be the year AMD truly stakes its claim in the AI market.

To conclude, around April, I saw AMD as a great buying opportunity. I was able to average down and pick up more shares of a forward-thinking company at an attractive price. Since those April lows, the stock has risen about 220%, and my position is currently up around 110%. AMD was a perfect example of a company moving in the right direction, even when the stock price was temporarily going the other way. Moments like that really test your conviction — you have to trust what you own. AMD is a company I plan to hold for the long term, and I see it as a core position for many years to come.

dLocal is currently my fourth-largest holding. It’s a global cross-border payments platform that helps international companies accept and send payments in emerging markets. I first bought the stock in May 2025, and as of now I’m up about 23% on the position. It’s a company I’m keeping a close eye on this year, and I look forward to each earnings period.

To be honest, I thought I’d be slightly higher on this position by now, as I still view the stock as undervalued. Because of that, I’ve been slowly increasing my position since the start of the new year. I’m hoping 2026 is a bigger year for the company, even though it finished last year up 17%.

This is another stock I’m happy to hold for the foreseeable future. The fundamentals remain strong, and the company continues to grow. While it isn’t without market volatility, dLocal is structurally well-positioned for the long term in global cross-border payments.

Adobe is a newer position for me. I started buying into the stock around early November last year, as it’s a position I want to build going into 2026.

2025 was a year to forget for the stock — not because of the business itself, but because the share price fell over 35% and has continued that trend into the start of this year. I spoke more about Adobe in my last post, where I made it my number one pick for a rebound in 2026.

The biggest fear — and what’s driven the sell-off — is AI. There’s a concern that many new tools can now do what Adobe has done for years, sometimes with what feels like “one click of a button.” While that might sound convincing on the surface, I don’t agree. Adobe is actively building out its AI infrastructure through Firefly, which has delivered positive guidance after every earnings quarter so far.

This is still a growing business, and throughout last year Adobe beat expectations every single quarter. Because of that, I struggle to justify the continued decline in the stock price, so I’m happy to keep buying at these levels.

It’s giving me strong Google-last-year vibes — a company moving in the right direction, beating earnings, investing heavily in AI, yet the market keeps pushing the stock lower. With Google, that disconnect gave me a doubled return in just six months.

As it stands, I’m currently down around 12% on my Adobe position. With earnings season coming up, I’m looking forward to seeing the results. This is a company I’ll continue to buy at these levels unless something materially changes. For now, despite all the negativity around the stock, the fundamentals — from what I can see — remain positive.

Churchill Capital (CCCX) is a special purpose acquisition company (SPAC), meaning it doesn’t run a normal business. It raises money through an IPO with the aim of merging with another company and taking it public without the traditional IPO process.

I bought into this stock toward the end of October last year. After the AI boom, I started thinking about what could be the next major technological wave. One sector that stood out to me — and had a strong year last year — is quantum computing. Despite that performance, I still believe the sector is in its very early stages.

While researching opportunities in this space, I came across CCCX. After digging into its plans and potential merger targets, I found that it is currently in the process of merging with quantum technology company Infleqtion. If completed, this merger would transform CCCX from a shell company into a fully operating business.

Although the deal appears likely to go ahead, there is still a chance it doesn’t. Because of that, this isn’t one of my largest positions. If the merger is completed, I’ll reassess and decide whether I want to add to the position going forward.

Quantum computing and quantum technology are areas I’m very bullish on long term. I believe this sector has the potential to be the next big thing over the next 5–10 years, similar to what we’ve seen with the AI boom in 2025.

Looking into the quantum space, I’ve been checking out companies like IonQ, D‑Wave Quantum, and Rigetti Computing. These stocks had a strong 2025, but after a pullback of around 40% from their October highs, their valuations felt a bit stretched. Considering this, it made sense to explore investment opportunities in the sector. Even though these companies performed well last year, none of them are actually profitable yet, so the pullback wasn’t too surprising. Much of their rally was driven by bullish market sentiment and investor FOMO, betting on future profitability.

Like its peers, Infleqtion isn’t profitable yet, but it already has commercial sales — including three quantum computers and hundreds of quantum sensors — something many competitors don’t have. With $29 million in revenue, its diversified product base (quantum sensors + computers) outpaces several peers.

Another reason I like Infleqtion is its smaller market cap compared to most public quantum tech stocks, which gives it potential upside if the SPAC merger completes. Compared to peers, it’s ahead in revenue generation and product diversity, while still being early-stage relative to large tech players.

Infleqtion also partners with big names like NASA, the U.S. Department of Defence, the UK government, and NVIDIA, using its quantum sensing tech in GPS-denied environments — making it extremely useful for defence, critical infrastructure, and research. On top of that, it has a growing pipeline of customer contracts, meaning it’s more than just a lab-stage company.

Overall, the quantum sector is starting to see real commercial deals. Big tech companies aren’t pure quantum plays, but many are heavily investing in quantum research and platforms, often tied to cloud or AI. For example, Google is exploring its quantum division and has already achieved early breakthroughs like quantum supremacy.

My current position in CCCX is down about 17%, but it’s a stock I plan to hold long term. If the Infleqtion merger goes through early this year, I expect the stock to perform well over the coming years, as it’s a company I believe is making all the right moves and a sector, I’m extremely bullish on.

Pagaya Technologies is an Israeli American financial technology (fintech) company that uses AI and machine learning to transform how credit decisions are made in the financial services industry. It operates behind modern lending, helping banks and fintech’s approve loans faster and more inclusively while connecting that lending to institutional investors.

I first invested in Pagaya in September last year, and its most recent earnings report was very positive, which has given me the confidence to hold the stock long term. At current prices, I believe the company is significantly undervalued. With its next earnings report coming up next month, I’m looking forward to seeing how the business has progressed since the last update.

This is a stock I’ll be following very closely in 2026 and one I want to continue learning more about. After the upcoming earnings report, I plan to do a deeper dive into the business. Based on its last report, I believe Pagaya is making the right moves, and the stock has been sold off far more than justified.

I’ve been accumulating more shares throughout this year, and while it’s still a relatively small position in my portfolio and currently down around 30%, I believe the stock is due for a rebound if the company continues to build on its recent performance.

Ondas Inc (ONDS) is a U.S.-based tech and defence company that focuses on things like autonomous systems (including drones), wireless communications, and robotics. Its customers are mostly industrial companies, government agencies, and defence organisations. In early 2026, the company changed its name from Ondas Holdings Inc. to Ondas Inc. to better reflect what it does today.

Ondas isn’t a consumer drone brand Instead, it builds industrial and mission-critical technology—such as autonomous systems and secure wireless networks—used for security, data collection, and communications in tough, real-world environments.

I first bought this stock in October, and when it dipped by around 45% in November, I saw it as a great opportunity to lower my average. The main reason I bought this stock was that I wanted exposure to the drone sector in my portfolio—but not just a company focused on commercial use. I was looking for a business with broader applications, particularly within the defence sector.

As this was a new position for me, I was initially sceptical. I didn’t know a great deal about the company at the time, and it’s one I want to understand much better heading into 2026. Before buying, I noticed that its previous two earnings reports had missed on EPS, and only the June report beat revenue expectations. That said, I could still see clear progression. However, I wanted more clarity, so I waited for the September update before committing.

That earnings report exceeded both EPS and beat revenue expectations by 43%, which ultimately gave me the confidence to start a small position. Looking back, I do wonder why I didn’t begin building my position earlier, as the company had already been securing deals and showing consistent progress in prior reports. But that’s one of the lessons I’ve learned over the years—you can’t time the market. You only buy when you believe the stock is trading at a price, you’re comfortable with and when the risk-to-reward makes sense.

As of now, following strong earnings and the November sell-off that allowed me to add more, I’m up 31%. I believe this stock has the potential for a strong 2026, and I’m looking forward to seeing how future earnings play out.

Terrestrial Energy is an advanced nuclear company building a new kind of small modular reactor. They use Generation IV molten salt technology called IMSR to deliver reliable, low-carbon power and high-temperature heat for industry and electricity generation. IMSR technology — molten-salt reactors that use liquid fuel/coolant mixes instead of traditional water-cooled designs. This allows higher operating temperatures, inherently safer low-pressure operation, and potentially more efficient, flexible deployment. Recent news the company is working with the U.S. Department of Energy on pilot projects to help develop its reactor design and fuel supply.

I bought this stock back in October before it merged to become Terrestrial Energy, similar to what’s happening now with my other stock, CCCX. At the time, I had a feeling I didn’t want to miss out in case it rallied after the merge—but the exact opposite happened. At one point, I was down 70% on my position.

Recently, with the news that the company is working with the U.S. Department of Energy, and with world leaders at Davos talking about the growing need for energy, the stock has rallied around 80% since that announcement. Before this news and the convention, I was slowly buying more shares while down 60–70%.

As someone who has worked in the nuclear industry, I’m extremely bullish because I believe nuclear energy is the best renewable source for the future. I’ve always wanted to invest in this sector, though I was hesitant at first given the unclear past stance of the Trump administration on nuclear. He had previously raised concerns about safety, but this week at Davos, he acknowledged the potential of nuclear energy. That made me both happy and more confident as an investor in this space.

Right now, my position is still down 50%, but it’s a long-term hold for me—at least five years. I’ll continue to watch the progress of this stock and the sector closely, especially as more investment flows in.

With AI and chips, Elon Musk mentioned that production might soon exceed what can be used. This highlights a major limitation for further AI development: the need for more reliable electrical power. Nuclear energy could play a key role in meeting that demand.

Although I believe nuclear energy is fantastic and will likely be the biggest renewable energy source in the coming years, I also want to give a quick shoutout to solar. I think this sector still has a lot of room to grow, both now and in the future, alongside nuclear. Two stocks I like in this section are Enphase Energy and T1 Energy.

Again, this is a stock I spoke about in my last post and my second pick I mentioned as a potential bounce-back for 2026. I’ve owned this stock before a couple of years ago and made around a 50% return. I recently bought back in toward the end of 2025 after seeing the price drop into $50 range. After strong earnings report late last year and the announcement of a deal with OpenAI, I couldn’t help but add it to my portfolio again. I’ll keep this brief since I covered it in more detail in my last post, but in short, the company seems to be transitioning well with the modern world. I also like how the CEO operates and his long-term vision for the business. At the moment, I’m slowly building my position again, so it’s not a large holding yet, but it will be if the stock remains around these levels. I’m currently down about 4%, but this is a position I’m holding into 2026.

KULR Technology is a U.S.-based company focused on battery safety, energy storage, and thermal management, particularly for lithium-ion batteries used in demanding industries. Its core goal is to make batteries safer and more reliable by controlling heat and preventing failures like thermal runaway, which can cause batteries to overheat or catch fire.

KULR also builds complete battery systems, not just safety components, through its modular KULR ONE platform. These are used in electric vehicles, grid storage, data-centre backup power, and aerospace and defence, combining safety technology with battery management and structural design.

Beyond batteries, the company has expanded into industrial robotics and AI, and it has also adopted a Bitcoin treasury strategy, investing a portion of its excess cash into Bitcoin as part of its financial approach.

I bought this stock in December 2024, and honestly, it’s been my biggest mistake—and lesson—since I started investing. I had been watching the stock closely throughout December and thought it was an interesting company, but I only did a surface-level review and didn’t fully understand everything that was going on with the business.

At the time, I had a healthy cash pile. When I first bought in, I kept the position small, which in hindsight was the right move. However, as the stock started to decline, I made the mistake of chasing it down week after week, buying on every red week and hoping for a turnaround instead of reassessing my thesis.

Looking back, there were other stocks I was interested in—such as Rocket Lab and Nebius Group. Instead of going all in and effectively gambling on one position, I should have spread my risk and split my investment across all three. That’s the most frustrating part, as Rocket Lab and Nebius went on to have outstanding year and I would have more than doubled my initial investment.

I’ve taken 2025 as a major learning year, and I’m keeping this stock as a reminder of that lesson. I still like the business, but I bought far too much of it, and at this point it’s too far gone for me to add any more. I won’t be investing further into it.

I’m currently down 89% on KULR. While it’s technically still my third-largest position by money invested, the heavy loss means it now sits much lower in my portfolio.

To conclude, in my second-ever post I wanted to outline my plan heading into 2026. The reason for doing this is simple: I want a written record I can look back on at the end of the year—and in years to come—to see where my investments stood and whether my thinking at the time was right or wrong. It’s something I’ve wanted to do for a long time but never got around to, and at the start of this year I finally decided to make it one of my New Year’s resolutions.

My plan for 2026 is to keep learning—reading more about stocks, doing deeper research, and taking a greater interest in world affairs. Over the past year, this has become increasingly important to me, not only because it impacts my investments, but also because of the state of the country I live in and how the government is operating.

From a portfolio perspective, my goal is to stay patient and allow my larger positions time to grow. I also want to rebalance my holdings so that by 2027 I’m less exposed to any single stock and have a more evenly spread, lower-risk portfolio overall.

I’ll revisit this post in December to see where my positions stand, and I hope to continue posting like this throughout the year—sharing thoughts, ideas, and deeper dives into individual stocks as they come to mind. I’ll leave it there for now. I hope this has been a good read for those who took the time, and that this becomes a regular thing I do at the start of each year.

David, I’m going to be honest up front. I understand approximately twelve per cent of this, and that’s on a good day with strong coffee.

But what I do understand is the thinking behind it, and that’s the impressive bit.

You’re not punting. You’re not chasing hype. You’re explaining what you own, why you own it, what you got right, what you got wrong, and what you’re still unsure about. Most grown adults never learn to think that clearly about anything, never mind money. And most never talk about or hare it either so well done you.

I especially loved that you’re honest about mistakes. That’s the bit that tells me this isn’t ego or gambling dressed up as confidence. It’s discipline. Curiosity. And a willingness to learn in public, which takes more bottle than people admit.

Whether every stock flies or some fall flat on their face is almost beside the point. You’re building judgement, patience and long-term thinking. That skill transfers to everything in life.

Also, the fact you’re writing it all down so future-you can look back and say “what was I thinking?” is quietly genius. Most people only do that after the fact and usually while panicking.

So no, I can’t advise you on quantum chips or AI accelerators, but I can say this. You’re doing something thoughtful, disciplined and far beyond your years.

Keep going. Stay curious. Stay humble. Don’t let a good year make you cocky or a bad one make you quit.

And if nothing else, I’m extremely proud to be related to someone who can lose 89 per cent on a stock and still write about it calmly rather than throwing their laptop out the window.

That alone deserves respect.

❤️